Live ARR is the SaaS metric most boards report and most decks confuse. The “live” qualifier matters because Annual Recurring Revenue actually has four common variants (live or recognized, booked, contracted or CARR, and pipeline), and each one produces a different number from the same customer base. Get the wrong one in your investor deck and the headline figure overstates reality by 10-20%. Get the right one and you have the cleanest revenue number a SaaS company can report.

This guide defines live ARR the way the SaaS Metrics Standards Board defines it, walks through the two formulas public companies actually file with the SEC, gives three worked calculation examples, and disambiguates live ARR from the three variants people most often confuse it with. By the end you should be able to recompute your own ARR with confidence and explain the methodology to a board in two sentences.

Key Takeaways

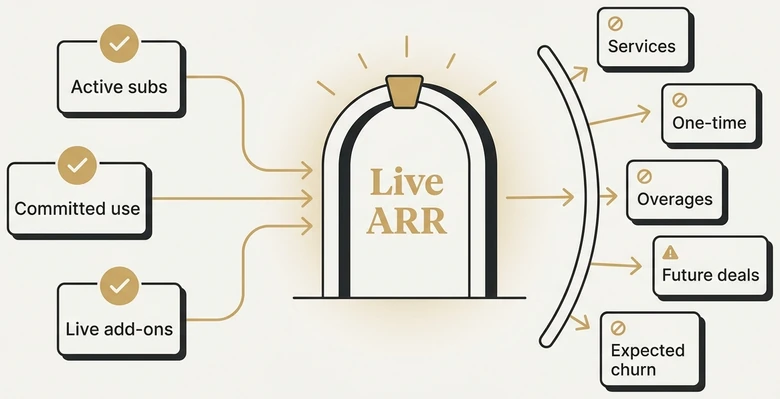

- Live ARR (also called Recognized or Realized ARR) is the annualized run-rate of recurring subscription revenue from active contracts at a measurement date, calculated under your revenue recognition policy. It excludes one-time fees, professional services, usage overages, and signed-but-not-yet-active contracts.

- Two formulas dominate filings: MRR × 12 (the SaaS Metrics Standards Board’s canonical formula) and sum of active contract ACV. Both produce the same number when applied consistently to subscription revenue.

- Live ARR is a point-in-time metric (like a balance sheet item), not a period metric (like income-statement revenue). One quarter’s ARR snapshot is not the same as that quarter’s GAAP revenue.

- The four ARR variants (live, booked, CARR, pipeline) answer different questions. Stripe’s billing documentation defines them as a timeline: recognized shows the present, ARR shows the run rate, committed shows the secured future.

- Investors discount any ARR figure that bundles managed services, usage overages, or future contracts. The premium NTM revenue multiple historically associated with top-decile public B2B SaaS sits around 10× and applies almost exclusively to clean live ARR.

What Is Live ARR?

Live ARR is the annualized value of all active subscription contracts at a specific measurement date, calculated under the company’s revenue recognition policy (typically ASC 606 for US GAAP filers) and excluding non-recurring revenue streams. The “live” qualifier separates this from booked ARR (signed but not started), CARR (live plus contracted future expansion), and pipeline ARR (weighted-probability open opportunities). Stripe’s billing documentation calls this Recognized ARR and notes it is “a live metric that focuses on revenue that’s currently being earned under revenue recognition accounting standards.”

The SaaS Metrics Standards Board takes the strictest position: live ARR should not include any future events (signed contracts that have not yet started, expected expansion, expected churn) and should exclude one-time fees and professional services even if those services recur. The Standards Board treats live ARR as a point-in-time metric, much like a balance sheet item, rather than a period metric like income-statement revenue. That framing matters when reconciling ARR to GAAP, where the two should agree directionally but never exactly.

IMPORTANT

If your reported ARR includes contracts that have not yet started delivering revenue, you are reporting CARR (Contracted ARR), not live ARR. Investors who catch the discrepancy will discount the headline number heavily and may reset the multiple they apply to it.

How to Calculate Live ARR: Two Formulas Public Companies Use

Public-company filings reviewed across 160+ SEC documents (notably by Ben Murray of The SaaS CFO in 2025 and the SaaS Metrics Standards Board in its standards work) converge on two subscription-ARR formulas, with a third pattern for usage-based revenue. The choice between them changes the reported number by 3-12% depending on contract mix.

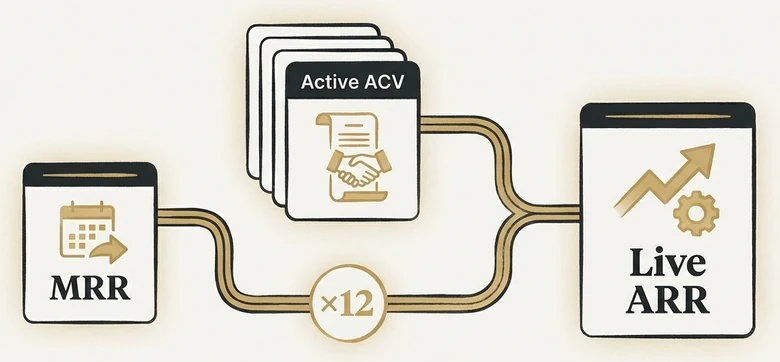

Formula 1: MRR × 12 (the snapshot method)

The SaaS Metrics Standards Board treats this as the canonical formula. Take the most recent month’s recurring revenue and multiply by 12. Clearwater Analytics describes this in its filings as “dividing the recurring revenue in the last month of such period by the number of days in the month and multiplying by 365,” which is the same idea with daily precision. This is the dominant approach for month-to-month subscriptions, annual auto-renewals, and any business where contract value tracks closely to monthly run rate.

Live ARR = MRR (most recent month) × 12Formula 2: Sum of Active Contract ACV (the contract method)

The contract method sums the annualized contract value across every active subscription, taking the per-year obligation rather than the recognized-revenue snapshot. AvePoint’s filings define ARR as “the annualized sum of contractually obligated Annual Contract Value (ACV) from SaaS, term license and support, and maintenance revenue sources from all active customers at the end of a reporting period.” This handles multi-year contracts more cleanly because it doesn’t double-count revenue across years.

Live ARR = Σ (ACV of all active contracts) at measurement date

The third pattern: usage-based annualization

For companies with consumption-based revenue, a third pattern emerges: annualize the trailing 30, 60, or 90 days of actual consumption. MongoDB’s 10-K annualizes the prior 90 days for direct-sales customers and the prior 30 days for self-serve. Confluent uses 90 days for Cloud revenue. The shorter SMB window can pump up reported ARR during seasonal usage spikes, which is why this method needs cohort-level disclosure to be defensible.

Three Live ARR Calculation Examples

Three worked examples cover the most common SaaS scenarios. Each starts with the standard inputs and produces a defensible live ARR figure.

Example 1: Annual subscription business

A SaaS company sells a $1,200/year subscription. It has 100 active customers on the plan as of the measurement date.

100 customers × $1,200 ACV = $120,000 live ARRThis is the cleanest case. The contract value already reflects yearly revenue, so the sum equals annualized run rate.

Example 2: Monthly subscription business

A SaaS company charges $100/month per customer. It has 50 active customers in the most recent full month, generating $5,000 MRR.

$100 × 50 customers = $5,000 MRR → $5,000 × 12 = $60,000 live ARRThe MRR × 12 formula handles month-to-month and annual auto-renew contracts identically.

Example 3: Mixed business with expansion and churn

A SaaS company starts the year at $100,000 ARR. Existing customers expand by $20,000 (upgrades, seat additions). $15,000 of ARR churns (cancellations and downgrades).

$100,000 starting + $20,000 expansion − $15,000 churn = $105,000 live ARRThis is the most realistic operating-business view. Expansion and churn are reported as distinct ARR movement categories, typically broken into five buckets: New, Renewal, Expansion, Contraction, and Lost.

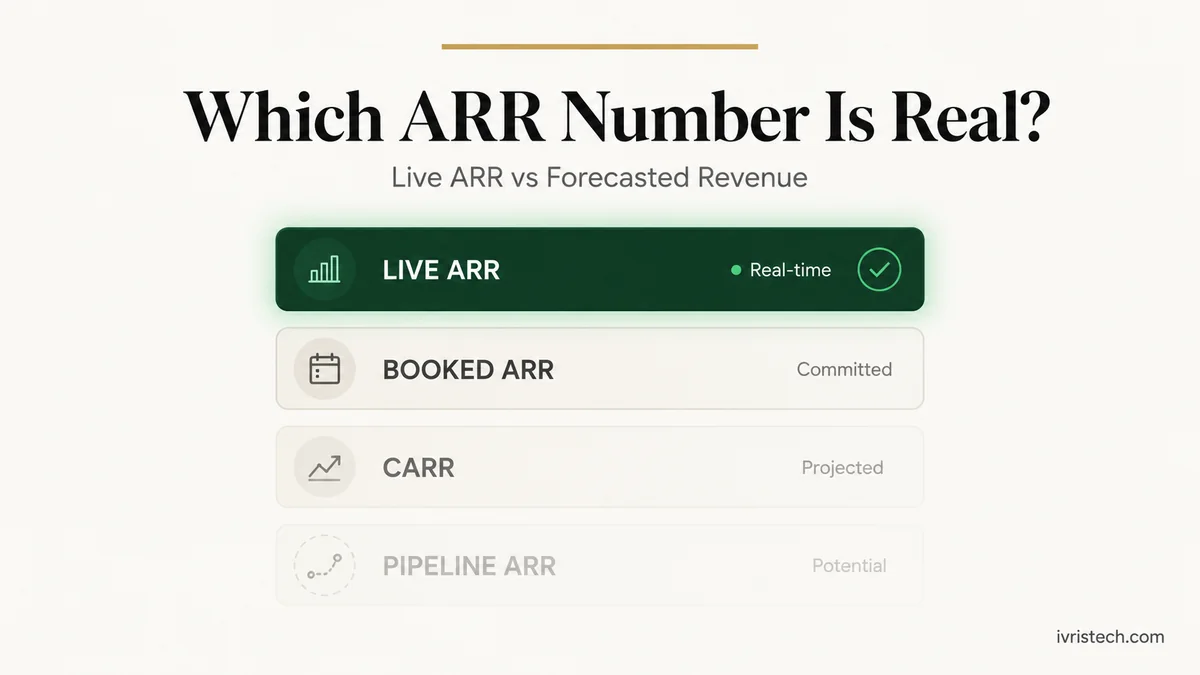

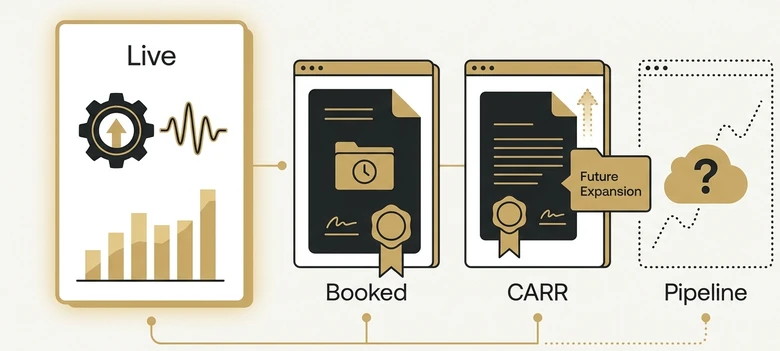

Live ARR vs Booked ARR vs CARR vs Pipeline ARR

The four ARR variants exist because finance, sales, and CS teams each track different things at different points in the customer lifecycle. The variants are not interchangeable, and putting the wrong one in an investor deck is the kind of mistake that costs trust faster than missing a quarter.

- Live ARR (Recognized ARR): Active contracts, currently delivering revenue, currently being invoiced. The most conservative and defensible variant. This is what Stripe’s documentation calls Recognized ARR and what the SaaS Metrics Standards Board treats as the strict ARR standard.

- Booked ARR: Signed contracts including those that haven’t started. As soon as a deal closes, its full annualized value is included. Useful for sales forecasting; misleading as a valuation input. Booked ARR can overstate reality if deals stall, get delayed in implementation, or fall through.

- CARR (Contracted ARR): Live ARR plus contracted future expansion (price escalators, ramp-ups, committed seat additions, signed renewals), minus known future churn. Sits between booked and recognized ARR. Useful for forward planning; not a public-reporting number.

- Pipeline ARR: Weighted-probability value of open sales opportunities. Sales-team metric for forecasting. Should never appear in a finance disclosure under any circumstance.

The distinction that matters most to readers of B2B SaaS financials is live vs. booked. A company reporting $10M in booked ARR with $7M actually delivering revenue has a 3-month gap between bookings signal and run-rate generation, and that gap is where pipeline-quality questions start.

ARR vs MRR: When to Use Each

ARR equals MRR × 12, but the two metrics serve different operational purposes. ARR is preferred by B2B SaaS with annual or multi-year contracts, lower transaction volume, and higher contract values. MRR is preferred by month-to-month subscription businesses, B2C SaaS, and any company optimizing operationally on a monthly cadence. Companies that track both tend to treat ARR as the valuation metric and MRR as the operating metric.

A practical rule: if your minimum contract term is 12 months or longer, lead with ARR in board reporting. If you have meaningful month-to-month volume, keep MRR as the primary operating metric and report ARR as the annualized view. Most billing platforms (Maxio, Chargebee, ChartMogul) and CRM-attached revenue tools (HubSpot Revenue Reporting, Salesforce CPQ) expose both metrics for this reason.

What Live ARR Includes and Excludes

The single most-impactful clarity move for any ARR disclosure is the inclusion and exclusion list. The SaaS Metrics Standards Board’s strict standard:

- Include: Annualized recurring subscription fees from active contracts; contractually committed minimum usage; recurring add-ons and seat expansions already in force

- Exclude: Professional services (even if they recur); one-time fees (setup, training, migration credits); usage overages above committed minimums (regardless of whether invoiced); signed contracts not yet generating revenue; expected churn or expected expansion not yet contracted; one-time customer credits

The exclusion that catches teams most often is the usage-overages line. Public companies like Datadog, Snowflake, and Confluent generate meaningful overage revenue, but the Standards Board’s position is that overages should not count toward ARR even when they’re being invoiced, because they’re not contractually committed and could disappear next month. Companies that bundle overages into headline ARR get it back as a discount in the multiple.

Live ARR Benchmarks by Stage and Growth Rate

ARR benchmarks shift with stage and category. The rough public ranges for B2B SaaS:

- Pre-seed: $0 – $200K live ARR; growth rate not yet meaningful

- Seed: $200K – $1M live ARR; investors want to see weekly or monthly growth velocity

- Series A: $1M – $3M live ARR with growth at or above 3× year-over-year (the “T2D3” benchmark of triple, triple, double, double, double)

- Series B: $5M – $15M live ARR with growth at or above 2× year-over-year

- Late stage / pre-IPO: $50M+ live ARR with sustained 30-50% growth and net dollar retention above 110%

A study of 439 SaaS companies cited in Maxio’s Saaspedia put the median ARR growth rate between 40% and 60% across all stages, with early-stage businesses ($1-3M ARR) sustaining higher growth than late-stage ($15M+) businesses. The top quartile of public-SaaS growth requires sustaining a rate above 100%. Vertical SaaS and infrastructure tend to clear lower growth bars in exchange for higher net dollar retention because their cohort retention is more predictable.

Why Live ARR Matters for Valuation and Board Decks

Live ARR sits at the center of every SaaS valuation framework. Public B2B SaaS trades primarily on a multiple of next-twelve-months revenue (NTM revenue), and the historic premium multiple for top-decile companies has hovered around 10× NTM revenue. Pure-subscription live ARR earns that multiple more easily than hybrid-revenue ARR because it’s the version analysts can defend without methodology footnotes.

Live ARR is also the denominator (or numerator) for nearly every other SaaS metric a board cares about: CAC payback divides marketing spend by new ARR added; the Rule of 40 sums ARR growth rate and EBITDA margin; net dollar retention compares this period’s ARR from the same cohort against the prior period’s. The metrics framework that surrounds ARR only works when ARR itself is defined consistently. Get the definition wrong and every downstream metric (LTV, CAC payback, NRR, GRR, Rule of 40) tells the wrong story. Parloa’s $50M-plus ARR update pairs the scale metric with 150% NRR, a useful reminder that ARR quality depends on cohort expansion as much as headline size.

Live ARR also intersects with pricing model design. Companies running usage-based or consumption pricing face the hardest definitional choices because the “recurring” qualifier blurs when revenue varies month to month. Pure-subscription pricing makes ARR easy and limits upside; usage pricing increases upside and makes ARR contestable. Snowflake, the canonical pure-consumption SaaS, does not formally define ARR in its filings for this reason.

Common Live ARR Mistakes That Tank Valuation

Five errors show up repeatedly in private-SaaS reporting and erode investor trust faster than any other line in the deck. The pattern is consistent: companies inflate the numerator (count more revenue as “recurring”) rather than fix the denominator (improve actual retention).

- Counting professional services. Implementation fees and one-time consulting are not recurring. Excluding them is the single point of agreement across every public-company definition reviewed.

- Counting one-time fees. Setup fees, training packages, and migration credits are not subscription revenue. They get reported separately in well-run finance functions.

- CARR-as-ARR. Including the future expansion year of a 3-year ramp deal as if it were live revenue today. The disclosure is technically defensible if the methodology is spelled out, but most decks don’t spell it out.

- Stale annualization. Using last quarter’s MRR × 12 in a market where the current month’s MRR is lower. Run-rate metrics are only as good as the most recent run.

- Mixing methods within a period. Some segments calculated MRR × 12, others summed contract values. Auditors find this pattern almost immediately and the resulting restatement is what triggers loss of investor trust.

PRO TIP

The single best practice for ARR reporting is the one most decks skip: state the methodology on the same slide as the number. A line like “Live ARR = sum of ACV across active subscription contracts at quarter-end, excluding professional services and usage overages” eliminates 80% of the questions investors will ask next.

How to Grow Live ARR

Three operational moves shift live ARR over time, in roughly this order of impact:

- Reduce churn first. A point of churn reduction compounds into perpetuity; a point of new ARR is a one-time event. Churn pulls live ARR down faster than new bookings can lift it, so retention work delivers higher long-term ARR than acquisition work in most stages.

- Expand existing accounts. Net dollar retention above 110% means existing-customer expansion alone grows ARR even before new acquisition. Pricing model design, packaging tiers, and CS-driven expansion motions are the levers here.

- Acquire efficiently. CAC-to-ARR ratios matter more than gross new ARR. Funnel discipline that converts qualified pipeline into live ARR beats top-of-funnel volume every time. The CAC numerator in that ratio is where most teams trip up — the fully-loaded calculation typically lands 25 to 40 percent above the headline number teams report to their boards.

Operationally, the RevOps function that owns ARR reporting end-to-end is usually the right place to centralize the definition and the methodology document. Documenting the methodology so the same calculation runs every quarter is the operational discipline that separates a defensible ARR number from a flattering one.

Frequently Asked Questions

No. ARR is an annualized run-rate of recurring contract value at a measurement date, a point-in-time metric similar to a balance sheet item. Revenue is the actual amount recognized over a period under GAAP rules. A growing SaaS company can have $5M in live ARR and only $4.2M in trailing-12-month GAAP revenue because ARR captures the current run rate while revenue captures the historical sum.

The headline live ARR figure is reported gross of churn and expansion movement but net of contract-level discounts. New ARR, churned ARR, and expansion ARR are tracked separately so the board can see movement. The current run rate after all churn and expansion has settled into the active contract base is sometimes called net ARR by convention, but the SaaS Metrics Standards Board uses a single ARR definition and reports the movement categories alongside it.

Two formulas dominate. MRR × 12 (most recent month’s recurring revenue annualized) is the snapshot method preferred by the SaaS Metrics Standards Board and most private companies. The sum of active-contract ACV (annualized contract value across every live customer) is the contract method most public companies use. Both produce the same number when applied consistently to subscription revenue. They diverge for multi-year contracts under the TCV approach; pick one and document it.

The benchmark depends on stage and category. Seed-stage B2B SaaS typically raises with $200K-$1M live ARR. Series A targets are usually $1M-$3M live ARR with strong growth (3× year-over-year). Series B benchmarks sit at $5M-$15M live ARR. Vertical SaaS and infrastructure tend to clear higher bars on retention because cohort behavior is more predictable. NRR above 110% and GRR above 90% are the retention bars investors weight most heavily alongside the ARR figure itself.

Only the contractually committed minimum portion. The SaaS Metrics Standards Board explicitly excludes usage overages above committed minimums from ARR, regardless of whether those overages are being invoiced. Companies like MongoDB and Confluent annualize trailing 30-90 days of consumption to estimate the recurring portion. Pure-consumption revenue with no contractual floor is the hardest to defend as ARR; Snowflake doesn’t formally define ARR for this reason.

Definition is identical. Reporting cadence and disclosure rigor differ. Startups report ARR monthly or quarterly to investors with simpler methodology (often MRR × 12). Enterprise SaaS like Adobe or Atlassian reports ARR quarterly in earnings releases and 10-Q filings under stricter methodology footnotes. Rubrik’s S-1 on SEC EDGAR defines Subscription ARR as “the annualized value of our active subscription contracts as of the measurement date, based on our customers’ total contract value, and assuming any contract that expires during the next 12 months is renewed on existing terms.” That precision is the public-company standard worth modeling against.

Live ARR is the input both metrics depend on. Customer Lifetime Value (LTV) is roughly average ARR per customer divided by churn rate (then multiplied by gross margin). CAC payback measures months to recover Customer Acquisition Cost from new ARR added. Both calculations break if the ARR definition shifts mid-period; this is why teams that grow past Series A typically write a one-page methodology document and pin it next to every board report.