On April 24, Google committed up to $40 billion in Anthropic — $10 billion now at a $350 billion valuation, $30 billion milestone-tied, plus 5 gigawatts of Google Cloud TPU capacity over five years. Amazon added another $5 billion days earlier, and Anthropic pledged up to $100 billion on AWS for roughly 5 gigawatts of compute. On April 29, The Information reported OpenAI missed its Q1 2026 revenue target with projected $25 billion cash burn. Anthropic’s run-rate revenue exceeded $30 billion in March 2026, up from ~$9 billion at end-2025, with Bloomberg reporting a $800 billion secondary-market valuation and an October IPO under consideration.

Most coverage framed this as a tech finance story. Bloomberg and Reuters led with the Anthropic valuation. CNBC and the WSJ tracked the OpenAI angle. For B2B teams running AI line items inside SaaS contracts, marketing automation, and CRM, the actual news is simpler: the AI vendor stack you renew in Q3 2026 is being financed right now, and the procurement posture you need has already changed.

Our read: B2B teams that locked in AI vendor terms in 2024-25 wrote contracts assuming model providers would be financially fragile and pricing would only go up. April flips that. Anthropic’s growth and the Google plus Amazon backing make multi-cloud delivery (AWS Bedrock, Google Vertex AI) the realistic procurement default, not the edge case. OpenAI’s Q1 miss changes renegotiation leverage. The procurement workflow that made sense in February doesn’t make sense in May.

Key Takeaways

- Google committed up to $40B to Anthropic on April 24 ($10B at a $350B valuation, $30B milestone-tied), adding 5 GW of TPU capacity over five years.

- Amazon added $5B days earlier; Anthropic pledged up to $100B on AWS. Total committed AI compute now exceeds 11 GW across deals.

- OpenAI missed Q1 2026 revenue per The Information (April 29) with projected $25B cash burn, creating real renegotiation leverage at renewal.

- Anthropic ARR exceeded $30B run-rate in March 2026 with $800B secondary-market valuation and an October IPO under consideration.

- B2B teams should audit AI vendor concentration, add Bedrock/Vertex delivery to evaluations, and re-baseline 2026 AI line items against compute supply.

What Actually Shipped in the Last Seven Days

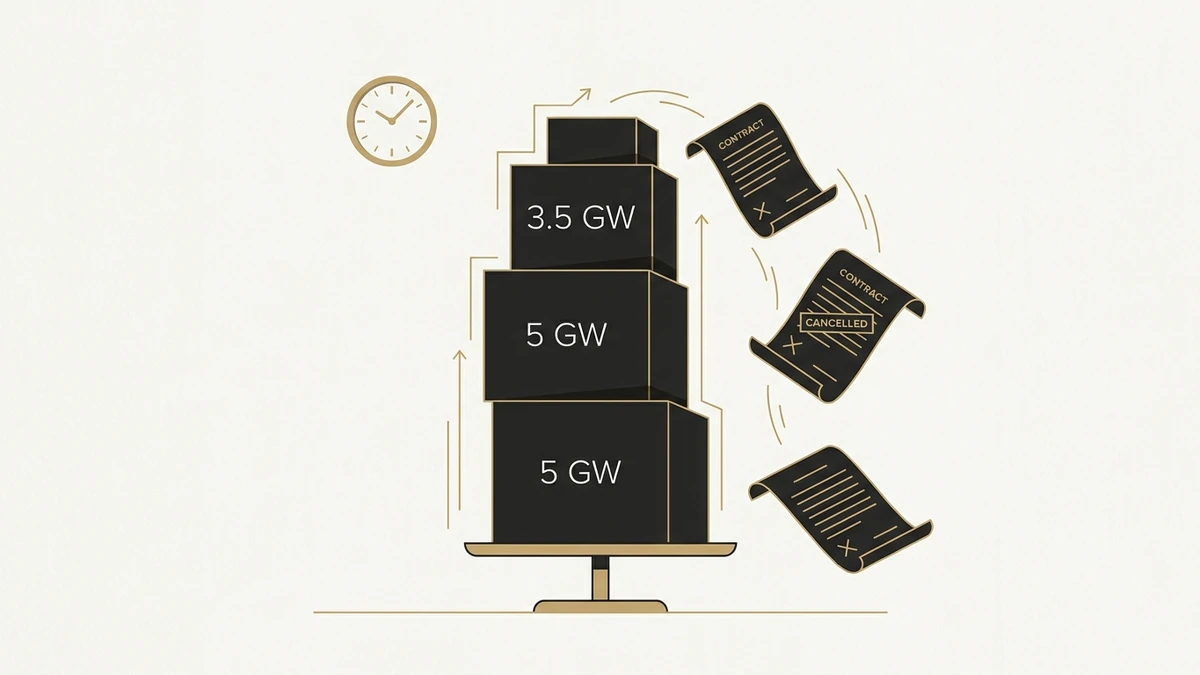

Three deals, one direction. Google Cloud will provide Anthropic 5 gigawatts of TPU capacity over five years, expanding a Broadcom partnership that brings another 3.5 gigawatts online in 2027. Amazon’s $5 billion is paired with Anthropic’s $100 billion AWS commitment for ~5 gigawatts of Trainium compute. Total committed AI compute across these deals now exceeds 11 gigawatts, equivalent to ten nuclear power plants.

The financial side moved faster than the infrastructure side. Anthropic’s run-rate revenue went from ~$9 billion at end-2025 to over $30 billion in March 2026, per Anthropic’s own April 20 Amazon announcement. That growth underwrites the secondary-market valuation surge to $800 billion and the October IPO conversation. OpenAI’s Q1 miss reported by The Information on April 29 is the other side of the ledger: aggressive growth assumptions written into 2025 enterprise contracts are now under pressure.

Why This Changes the B2B Procurement Conversation

Before the April deals, the case for a single direct API contract had two arguments: simpler integration, and vendor stability concerns favoring the largest provider. Both are weaker now. The April AI subscription reset already showed token-based billing migrating into B2B procurement; the compute supply increases visible across these deals confirm the pricing trajectory.

Multi-cloud model availability is the second shift. Anthropic’s Claude is on AWS Bedrock and expanding to Google Vertex AI; OpenAI’s models recently expanded beyond Microsoft Azure exclusivity to include AWS. Cloud-mediated delivery is the realistic path for SOC 2 compliance, data-residency commitments, and audit trails that direct API contracts can’t always match. ChatGPT Workspace Agents’ EKM exclusion made this concrete on the OpenAI side; Bedrock and Vertex are what closes that gap for security-sensitive workloads.

The third shift is on terms. Agentic AI buyers who signed in 2025 priced against a market where compute was scarce and vendors were funded in increments. The 11+ GW now committed says the next renewal cycle prices against a different market. Renegotiation leverage at renewal — usage-based billing tiers, multi-cloud options, clearer exit terms — is now actually negotiable. The SaaS-side analog Intuit just made public for Mailchimp reinforces the same posture from the demand side: when a vendor publicly confirms it is running a product for cash flow rather than growth, the procurement framework that treated platform stability as a tech-due-diligence checkbox needs a financial-stability column added next to it.

Three Procurement Moves for the Next 30 Days

Audit AI vendor concentration across your tech stack. Pull every vendor that uses model APIs underneath their UI: CRM, sales-enablement, customer-support, AEO and content-ops tools. Note the underlying model provider. If three or more critical workflows depend on a single provider, flag the concentration risk. Vendor financial stability is now part of due diligence, not just a tech question. The new Bedrock AgentCore Payments rail with Coinbase + Stripe adds a second concentration vector worth tracking: any tool that adopts agent-payment infrastructure is also adopting the wallet provider, the payment protocol, and the spending-control plane underneath it, all of which compound the vendor-stack dependency map procurement teams have to govern.

Add Bedrock/Vertex delivery options to your AI vendor evaluations. When evaluating or renegotiating AI-enabled tools, ask whether the vendor can deliver via AWS Bedrock or Google Vertex AI rather than direct API. Cloud-mediated delivery improves audit trail, data-residency posture, and SOC 2 / ISO 27001 documentation. For workflows touching customer-facing AI surfaces, that matters more than the small latency advantage direct API gives. The agency-holdco identity-layer parallel surfaced this week with Publicis-LiveRamp extends the same audit-trail logic to identity infrastructure: when the data-collaboration layer underneath ABM and clean-room measurement shifts ownership to a parent that also operates competitor-adjacent client portfolios, the data-flow attestation request becomes the identity-side equivalent of demanding Bedrock or Vertex delivery on the model side.

Re-baseline your 2026 AI line items against compute supply, not vendor scarcity. Most AI line items were built on a 2024-25 assumption that vendor capacity was the bottleneck. The 11+ GW committed reverses that for the second half of 2026. Renewal conversations should reflect the new posture: usage-based billing, multi-vendor fallback, clearer exit terms. Vendors who refuse those terms are pricing against a market that no longer exists.

The broader pattern: as Adobe ships MCP for Marketo and Salesforce ships Headless 360, B2B martech is converging on agent-addressable protocols. The Anthropic-Google compute deal is the supply-side bet behind those shifts. Teams that rebuild their AI vendor framework in May-June around multi-cloud delivery, financial stability, and compute-aware pricing will be in a different position at fall renewals.

Frequently Asked Questions

Up to $40 billion: $10 billion now at a $350 billion Anthropic valuation, with $30 billion to follow on performance milestones. The deal includes 5 gigawatts of Google Cloud TPU capacity over five years, expanding a Broadcom partnership that adds 3.5 gigawatts of TPU capacity starting in 2027.

No. The Information’s April 29 report on the Q1 miss and projected $25 billion cash burn is a renegotiation signal, not an exit signal. The practical implication is leverage at renewal: usage-based billing, multi-cloud delivery via AWS, and clearer exit terms are now negotiable.

AWS Bedrock and Google Vertex AI let enterprises access frontier models through their existing cloud provider rather than direct API contracts with the model labs. This brings the model into your existing audit, identity, and compliance stack — CloudTrail logging, IAM policies, data-residency commitments — which is hard to replicate via direct API.

Run-rate revenue exceeded $30 billion in March 2026, up from ~$9 billion at end-2025. Combined with $40B from Google, $5B from Amazon, and a $800B secondary-market valuation per Bloomberg, the financial-stability concerns that drove some 2025 procurement decisions look different now. Anthropic is no longer a vendor-concentration concern in the way it was 18 months ago.